The key technologies that are core to the energy transitions story are wind, solar, electric vehicles and battery storage. Both wind and solar have high critical mineral requirements. Solar has high requirements for copper and aluminium while wind energy has high requirements for rare earth elements, copper and zinc. Electric vehicles and battery storage have high demands for copper, cobalt, nickel, lithium, rare earth elements and aluminium. Even hydrogen energy has a high requirement for nickel and platinum group metals. According to the International Energy Agency, global clean energy transitions may result in doubling of mineral demand from clean energy technologies double in the Stated Policies Scenario (STEPS) and would quadruple in the Sustainable Development Scenario (SDS) ; in these scenarios, the deployment of electric vehicles and battery storage technologies is expected to account for about half of the mineral demand growth. Presently electricity networks account for a major portion of mineral demand in energy systems. In future, mineral demand will be driven by electric vehicles and battery storage.

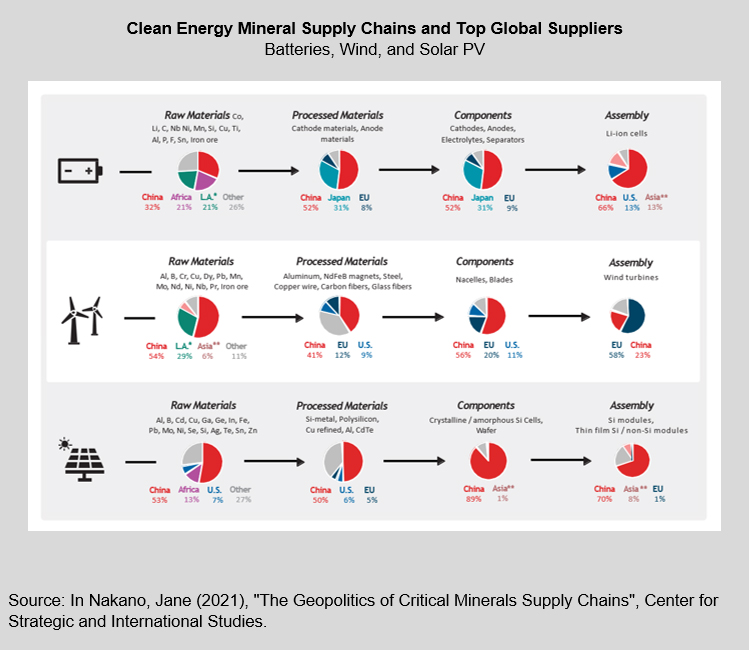

As the race for clean energy and net-zero intensifies, critical minerals supply chains will become a greater global strategic issue. The distribution of mineral availability is highly uneven and is concentrated in a few countries. About half the global supply of cobalt comes from the Democratic Republic of the Congo; over 80 percent of the global supply of lithium comes from Australia, Chile, and Argentina; and 60 percent of the global supply of manganese comes from South Africa, China, and Australia; and over 85 percent of the global supply of rare-earth elements comes from China . Resource security and ensuring an adequate supply of critical minerals strategic issue given the expected exponential demand growth led by clean energy technology deployment globally. China is not merely a consumer of raw minerals and materials but is a key consumer of them and has developed strong capacities in midstream and downstream segments of clean energy value chains. The image below is illustrative of China’s prowess across solar, wind and battery technologies.

As markets go bullish on clean energy technologies and pressure mounts to move away from fossil-fuel energy systems, governments across the world will intensify their efforts to deploy renewable energy technologies. This will also include efforts to address energy poverty and provide energy access. What will be implications of mineral insecurity on addressing efforts to address energy poverty? What will be other socio-economic implications in upstream areas where the mining of critical minerals take place? What will be the implications for material flow as well as circular economy measures? Goal 12 of the SDGs is concerned with natural resource use. In this regard a key question is how can the linkages between SDG 12 and SDG 7 be strengthened?

[Headline Question] How do we better factor ‘resource security’ in discussions around energy transitions and addressing energy poverty?

The session will start with brief 2-3 minute remarks by the Chair. The chair will then invite the speakers to deliver addresses of 8-minute duration. Based on issues emerging, there will a quick round of discussions involving the session chair and the speakers. The speaker will summarise the discussion and key answers to the question- “How do we better factor ‘resource security’ in discussions around energy transitions and addressing energy poverty?”. The speakers may choose to address all or a few questions. Strict time management is to be followed. There will be an on-screen timer.

The Energy & Resources Institute

6C, Darbari Seth Block, India Habitat Centre, Lodhi Road

New Delhi - 110 003 India

Email : wsds@teri.res.in

Ph. : +91 11 24682100 (Ext. : 2467)